If a real estate purchase agreement is missing clear names, a full property description, price terms, dates, or contingencies, the deal can fall apart. In the U.S., these contracts must be in writing and signed to hold up under the Statute of Frauds. And unclear property details were tied to 22% of delayed closings in 2023.

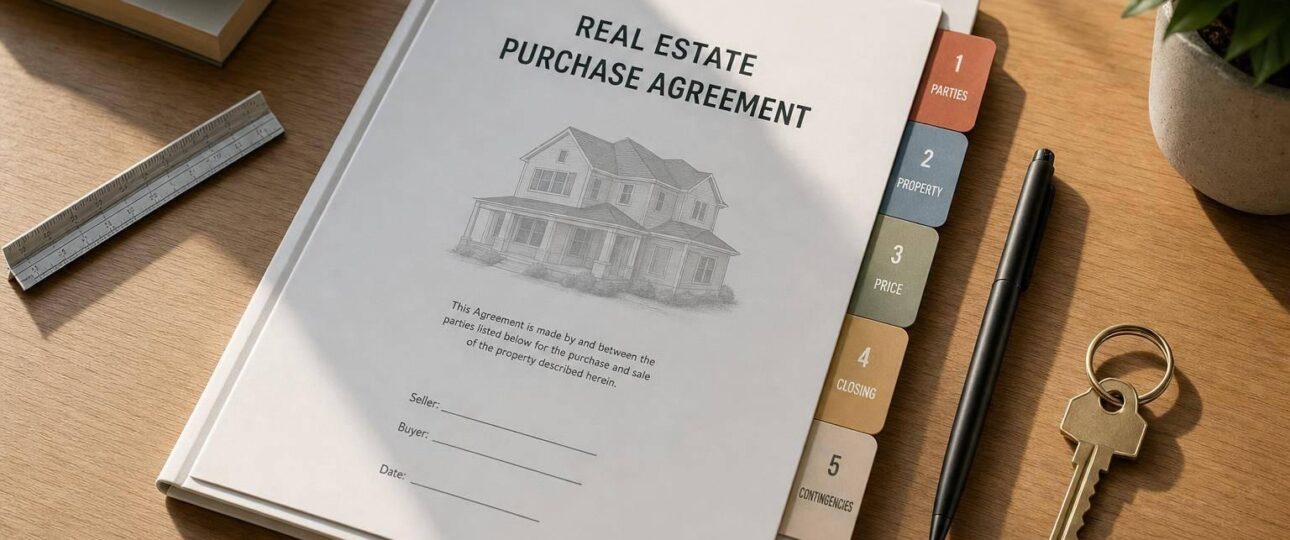

If I had to boil the whole article down, I’d say this: before anyone signs, I’d make sure the contract clearly covers these five parts:

- Buyer and seller details: full legal names and proper signing authority

- Property description: legal description, parcel ID, and what stays or goes

- Purchase price and payment terms: price, earnest money, loan terms, credits, and prorations

- Closing date and possession terms: when closing happens and when the buyer gets the property

- Contingencies: financing, inspection, appraisal, title, and home-sale deadlines

A few numbers matter right away:

- Earnest money often runs 1% to 3% of the purchase price

- Inspection periods are often 7 to 15 days

- Title cure periods are often 15 to 30 days

- Buyers must get the Closing Disclosure at least 3 business days before closing

5 Parts of a Real Estate Purchase Agreement: Key Terms & Deadlines

How To Write a Purchase Agreement for Real Estate [8 EASY STEPS]

sbb-itb-a688917

Quick Comparison

| Part | What it covers | Common problem if unclear |

|---|---|---|

| Buyer and seller details | Legal names, ownership form, signing authority | Title delays, bad signatures, ownership disputes |

| Property description | Legal description, tax ID, fixtures, included items | Confusion about what is being sold |

| Price and payment terms | Purchase price, deposit, financing, credits, prorations | Last-minute money disputes |

| Closing and possession | Closing date, recording, keys, move-out timing | Delayed move-in or access fights |

| Contingencies | Deal-exit terms and deadlines | Lost deposit or waived rights |

Bottom line: I’d treat the agreement as the written plan for the whole sale. If the terms are exact – names, numbers, dates, and notice rules – you cut down the odds of delays, deposit fights, and closing-day surprises.

What a Real Estate Purchase Agreement Actually Does

A purchase agreement doesn’t transfer title to a property. It sets the terms for that transfer. As ContractsCounsel puts it:

"A real estate purchase agreement doesn’t transfer the title of a property. Rather, it is the document that builds and creates a framework of the responsibilities of each party." [3]

Think of it as the written game plan for the deal. It guides the buyer, seller, escrow holder, title company, and lender from an accepted offer all the way to closing.

How a purchase agreement becomes binding

A purchase agreement becomes binding when one side makes an offer, the other side accepts those exact terms, and both parties sign the same version [5]. If one side sends back a counteroffer, the first offer is off the table. That means a binding contract exists only when both sides agree to identical terms [5].

The last signature sets the effective date. That date matters because it starts the clock on contingency deadlines [5].

How state and local rules affect the details

State law shapes attorney review, disclosures, deadlines, and closing procedures. So the agreement has to fit the rules where the property is located.

This is one reason real estate contracts can look similar at first glance but work a bit differently from place to place. The address may change, but the legal rules change too.

Why clear written terms prevent disputes

Vague language is where deals start to wobble. A contract should spell out exact dollar amounts, specific dates, and who handles what. When those terms are clear, both sides know what they agreed to.

It also helps to list fixtures, appliances, and any other included items in writing. If something is left out, it’s open to dispute.

Once that framework is in place, the agreement must identify the buyer and seller.

1. Buyer and Seller Details

Once the deal terms are clear, the next step is simple: name the parties correctly.

List every buyer and seller by full legal name, exactly as shown on the deed and in the planned title form. Even a small name mismatch can slow down title review and delay closing. Getting the names and signing authority right helps avoid title defects, closing delays, and ownership disputes.

This matters even more when the parties are not just one individual buyer and one individual seller. Married couples, co-owners, estates, trusts, LLCs, and corporations need to be listed the right way, and the person signing must do so in the proper legal capacity [4][10][11][12]. For example, a trustee should sign as trustee, not as an individual [10].

If a buyer or seller is an LLC or corporation, use the entity’s registered legal name in the agreement. The signer should also have documented authority to act for that entity, based on the operating agreement or other governing records [11][12]. That may sound like a small detail, but it can turn into a big headache if ignored.

When multiple buyers are taking title together, the agreement should also state how they will hold title, such as joint tenants or tenants in common, because each option affects ownership rights in a different way [8][7].

Before anyone signs, compare the agreement against the recorded deed and make sure every name matches exactly [10][4].

Once the parties are named the right way, the agreement must identify the property with the same level of precision.

2. Property Description

Once the parties are named the right way, the next job is to spell out the exact property covered by the contract.

A street address alone isn’t enough. You need the legal description from the deed or title commitment, copied exactly as written. That description controls what the contract covers, and even a small transcription mistake can lead to title issues and derail closing [5][10].

Put simply: the contract should match the property with zero guesswork.

The legal description usually appears in one of these forms:

- Lot-and-block

- Metes-and-bounds

- Government survey reference

The agreement should also include the parcel or tax ID number. And if the property is part of a condo or similar project, add any unit numbers, assigned parking spaces, and storage units too.

The purchase agreement also needs to say what stays with the property and what the seller plans to take. Fixtures, like built-in shelving, ceiling fans, and light fixtures, are usually included by default. Personal property, such as a freestanding refrigerator, usually is not. If an item sits in a gray area, list it on its own so no one has to argue about it later.

Before signing, check the description against the deed, title report, and county records. That extra review matters. In 2023, unclear or missing property details caused 22% of delayed closings [1].

| What to Verify | Where to Check |

|---|---|

| Legal description accuracy | Current deed or title commitment |

| Parcel/tax ID number | County assessor’s website |

| Recorded easements and encumbrances | Preliminary title report or county recorder |

| Fixture and personal property inclusions | MLS listing sheet and preliminary title report |

| HOA restrictions (if applicable) | CC&Rs and HOA bylaws |

With the property pinned down, the next piece is the purchase price and how payment will work.

3. Purchase Price and Payment Terms

Once the property is picked, the agreement needs to spell out exactly what the buyer will pay and how that money will be handled. This is where the deal’s main numbers live. It should state the full agreed purchase price before credits, concessions, prorations, and closing costs. It also needs to cover the earnest money deposit, payment method, down payment, financing amount, seller concessions, and how recurring costs are split at closing [4][9].

Earnest money is the buyer’s deposit to secure the deal. In residential sales, it usually falls between 1% and 3% of the purchase price and is often due within 1 to 3 business days after the contract is signed [9]. The agreement should name who will hold that deposit – often an escrow agent, title company, or attorney – and explain when the money is refunded or forfeited if the deal falls apart [5][14]. After that, the contract should lay out the financing setup that covers the rest of the price.

Financing type matters because different loan programs can bring different rules and deadlines [4][11]. For example, VA loans may require a VA Amendatory Clause [9]. The agreement should also list the exact down payment and financing amount so the cash due at closing isn’t a guessing game [7][6].

Before signing, check every dollar amount against the lender’s pre-approval. Also confirm that any seller credits stay within the loan program’s limits [4]. The contract should state how taxes, HOA dues, and utilities will be prorated, since the method used will change the final settlement amount [5]. When the numbers are clear on paper, there’s less room for last-minute fights over cash to close.

Once the price and payment terms are locked in, the contract needs to set the closing date and possession terms.

4. Closing Date and Possession Terms

Once the price and payment terms are set, the agreement needs to lock in the closing date and the possession terms. The closing date is when the papers are signed and the money changes hands. The possession date is when the buyer gets the property. Those dates often line up, but not always [13][6][15].

The contract should say, in plain terms, exactly when possession happens. That might be “upon closing,” “after the deed is recorded,” or at a set time on a set date [4][10]. It should also spell out how the buyer gets access, including:

One clause matters more than many people think: Time is of the Essence. That language makes the closing deadline strict. If someone misses it, they can lose rights under the agreement or even a deposit.

If the seller plans to stay in the home after closing, don’t leave that to a handshake deal. Use a written post-closing possession agreement, often called a rent-back. That document should cover daily rent, utilities, a security deposit, and penalties if the seller does not move out on time [4][10].

Timing details matter here. In some counties, possession does not happen the moment everyone signs because deed recording can take hours or even days. So before signing, confirm whether possession happens at closing or only after the deed is recorded [4][10].

There are a couple of practical checks worth making early:

- Schedule the final walkthrough within 24–48 hours of closing so you can confirm repairs are done and all included fixtures are still there [4][5].

- Check lender timing right away. Buyers must receive the Closing Disclosure at least 3 business days before closing, and major changes can delay the date [10].

With timing and possession pinned down, the agreement should next lay out the contingencies that let either side walk away if key conditions are not met.

5. Contingencies

Once the closing terms are in place, the contract needs to spell out what happens if something important goes sideways. That’s where contingencies come in.

A contingency is a contract clause that lets the buyer walk away without losing earnest money if a stated condition isn’t met. In plain English, it gives the deal some breathing room. If financing falls through, the inspection turns up a mess, the title has problems, or the appraisal comes in low, the buyer has a way out. Without that protection, a failed condition can leave the buyer in breach.

The most common contingencies are financing, inspection, appraisal, title, and home sale. Each one covers a different kind of deal risk:

- Financing: Lets the buyer terminate if their mortgage is denied or if loan terms change in a way that affects closing [15][5].

- Inspection: Gives the buyer a set window – usually 7 to 15 days – to inspect the property and ask for repairs, a price cut, or cancellation [15][5].

- Appraisal: Lets the buyer renegotiate or exit if the home appraises below the agreed purchase price [15][5].

- Title: Lets the buyer terminate if the seller can’t clear liens or encumbrances within 15 to 30 days [15][5].

- Home sale: Protects buyers who need to sell their current home first, though sellers often push back with a kick-out clause that gives the buyer 24 to 72 hours to remove it [5].

These clauses live and die by deadlines. They work a lot like closing and possession terms: if the contract says too little, trouble starts fast. Language like “within a reasonable time” sounds harmless, but it opens the door to fights later. A better move is to use exact dates or a fixed number of days.

The effective date matters just as much. It sets the starting line for every contingency clock, and getting that date wrong by even one day can cut an inspection window short in a way that matters [5]. The contract should also say whether deadlines run in calendar days or business days [4].

For each contingency, the contract should make three things clear:

- the exact deadline

- when the clock starts

- how notice must be delivered

Inspection language needs extra care. The contract should say whether the buyer may cancel for any reason during the inspection period or only for material defects. That one detail can change how much room the buyer has to act. If a deadline is missed, the buyer may waive the right to cancel and put the deposit at risk [15][5].

"Time is of the essence in these contracts. Deadlines for earnest money, inspections, and objections to title defects are strict. Miss one, and you may lose your rights or your deposit." – David Greiner, Esq., Greiner Law Corp [13]

The next step is to compare how the most common contingencies work.

Common Contingencies Side by Side

Each contingency covers a different risk. Each one also runs on its own deadline.

If you want the quick version, this table makes the main differences easy to spot.

Four common contingencies at a glance

| Contingency | What It Protects | Risk If Missing | Why Deadlines Matter |

|---|---|---|---|

| Financing | The buyer’s ability to secure a mortgage loan | The buyer may lose the deposit or face breach for failing to close | Lenders often need 21–30 days; missing the deadline can waive the right to exit if the loan is denied later [5] |

| Inspection | The buyer’s right to inspect the property and negotiate repairs, a price reduction, or termination if major defects are found | The buyer may miss major defects and lose leverage to negotiate repairs | Inspection windows are usually 7–15 days; missing the deadline can waive the right to object to defects [5] |

| Appraisal | Protects the buyer from overpaying if the home’s appraised value comes in below the offer price | The buyer may have to cover the appraisal gap in cash or the deal may fall through | Loan approval can stall until the appraisal is complete [2] |

| Title | The buyer’s right to clear title free of liens, boundary disputes, or ownership claims | The buyer may face disputes over liens, unpaid taxes, or legal battles over property rights | Sellers usually get a 15–30 day cure period to resolve discovered title defects [5] |

| Home sale | The buyer’s ability to close if they need to sell their current home first | The buyer may be in breach if their home does not sell in time | Sellers often respond with a kick-out clause giving the buyer 24–72 hours to remove it [5] |

Some risks are obvious right away. Financing and inspection usually get the most attention because they show up early and can derail a deal fast.

Title is different. It tends to stay in the background until something goes wrong. But when it does, it can stop closing just as fast as a loan issue or a bad inspection. And there’s the catch: even after a title search, hidden defects can still slip through. That’s why the title wording in the contract should stay specific.

Conclusion

A purchase agreement only does its job when the main terms are clear, complete, and signed. Those five sections turn a simple offer into an enforceable contract. If even one part is vague or wrong, the cost can add up fast.

The buyer and seller details, property description, price, closing terms, and contingencies all work together to keep the deal enforceable and moving on time. They cut down confusion at closing and help lower the chance of disputes. Put simply, they name the parties, define the property, set the price, lock in the timing, and spell out the contingencies – one system with five parts.

Before signing, cross-check names against the current title, verify the legal description with county records, and make sure each contingency includes a clear deadline. Clear terms at the start help protect both sides.

FAQs

What makes a purchase agreement legally binding?

A real estate purchase agreement becomes legally binding when it is in writing and signed by both the buyer and seller. That rule comes from the Statute of Frauds, which applies in all U.S. states.

But a signature alone isn’t enough. The agreement also needs to show a clear offer and acceptance. It must include consideration, involve competent parties who are of legal age and sound mind, and serve a lawful purpose. On top of that, it needs to clearly state the purchase price and the legal property description.

Put simply, the contract has to show that both sides agreed to the same deal, knew what they were signing, and put the key terms in writing.

What happens if a contingency deadline is missed?

If a contingency deadline is missed, what happens next comes down to the contract language. In some cases, it can trigger penalties, lead to the loss of earnest money, or cause the deal to fall apart.

After the deadline passes, the party tied to that contingency may still have a few options: waive the contingency, request an extension, or end the agreement. Miss one of these dates, and you could weaken key contract rights and lose protections that matter.

Can a street address alone identify the property?

No. A street address by itself is not enough for a real estate purchase agreement.

The contract should also include the property’s legal description. That may include the lot and block, parcel number, or a metes and bounds description. A street address helps identify the property, but on its own, it can leave too much room for doubt and may make the agreement hard to enforce.